Dentistry is evolving, creating huge opportunities for entrepreneurial dental professionals, provided they can access affordable and reasonably structured capital.

The trend toward large group practices and dental support organizations (DSOs) is not new. It is however rapidly advancing. Of the less than 200,000 dental offices in the United States, just 5% are currently a group practice or DSO, according to the American Dental Association. However, experts predict that this will reach 25%-30% by 2025 and almost 50% by 2030. Dentistry will increasingly operate in a corporate environment – some companies could potentially list on the stock exchange via IPOs.

There are many drivers of the shift towards DSOs. Increased competition is encouraging the dental industry to focus on operating efficiencies and margins. In addition, patient demands and expectations are growing. The availability of information anytime via the internet and smartphones has turned dental patients into wise consumers: they expect the latest technology, access to information via patient portals, and the ability to schedule appointments by smartphone or text messaging. Meeting these demands at a time of compressing margins is challenging. Inevitably, it has prompted consolidation in the industry.

Another driver of change is the shortage of skilled clinicians, which makes it tougher for small or solo dental practices to compete – larger organizations are often perceived as offering more attractive work environments and can offer better packages to recruit new dentists.

Studies show that newly graduated dentists are less likely to want to own a practice than previous generations. Instead, they would rather become a salaried employee with a predictable income and the freedom to focus on quality of life (and address their school debt). Working for a DSO or large group is also an attractive proposition for new graduates because they have few managerial or administrative responsibilities and can focus on their patients. This model is also beneficial for DSOs as newer dentists tend to be more skilled in the newest methods of treatment that are more likely to generate higher revenues.

The Challenge for the Middle Market

The disruptive trends described above present an opportunity to grow a successful group practice or DSO. But one thing stands in the way of capitalizing on this consolidation: cash.

Large corporations find it relatively easy to access capital: both middle market and corporate-focused banks and private equity (PE) firms compete to offer creative banking and financing solutions. As a result, large DSOs have been able to buy multiple locations and practices. At the same time, small solo practices or those with a couple of offices can count on the support of local and national banks when they need capital to acquire or start a dental practice.

The challenge is for practices between these two extremes – middle market group practices or emerging DSOs – which find it difficult to access reasonably priced capital. These entities, which typically have 5-50 locations, are too big for the dental lenders to support yet too small for corporate-focused banks. The irony is that these practices, which represent the majority of the group practice DSO landscape, arguably offer the greatest potential for growth.

This capital shortage has caught the attention of many PE firms, which have been heavily involved in helping DSOs grow. PE involvement has prompted a change in mindset in dentistry. Less than a decade ago, few dentists would have understood how to value a practice based on a multiple of earnings before interest, taxes, depreciation and amortization (EBITDA). Now EBITDA is avidly discussed at DSO conferences.

Providing an Alternative for Middle Market Group Practices and DSOs

The shortfall of capital for emerging and middle market group practices and DSOs means they face barriers to growth. This is especially true when they are in competition for practices with cash-rich corporate DSOs; typically the larger firms will be able to pay higher multiples than a small DSO can afford or is willing to pay.

Some middle market practices and DSOs may be able to secure PE capital, although this has both advantages and disadvantages. But the majority needs to bring together multiple lenders to fund acquisitions or the de novo strategy aspired to by some DSOs. This challenge has been compounded by the exit of two well-known regional banks in 2016 and 2017.

From a bank’s perspective, this type of lending is complex: most firms serving the health care sector focus on the ability of the dentist/owner to perform dentistry to generate cash flow. Loans are generally collateral light, so banks rely on cash flow to repay the loan; if the dentist/owner, who is the primary repayment source, cannot practice there is effectively no collateral. As a result, banks are often uncomfortable lending to DSOs when the dentists performing treatments are not the owners or part of the borrowing team. Such a scenario forces banks to evaluate hiring and retention arrangements.

Another complicating factor for banks, which lowers their appetite to lend, is the differing regulatory environment for the corporate practice of dentistry in each state. Lenders need significant industry expertise to understand and address these complex challenges and recognize areas where clients or potential clients have gaps in their operations, which could have risk implications for the bank.

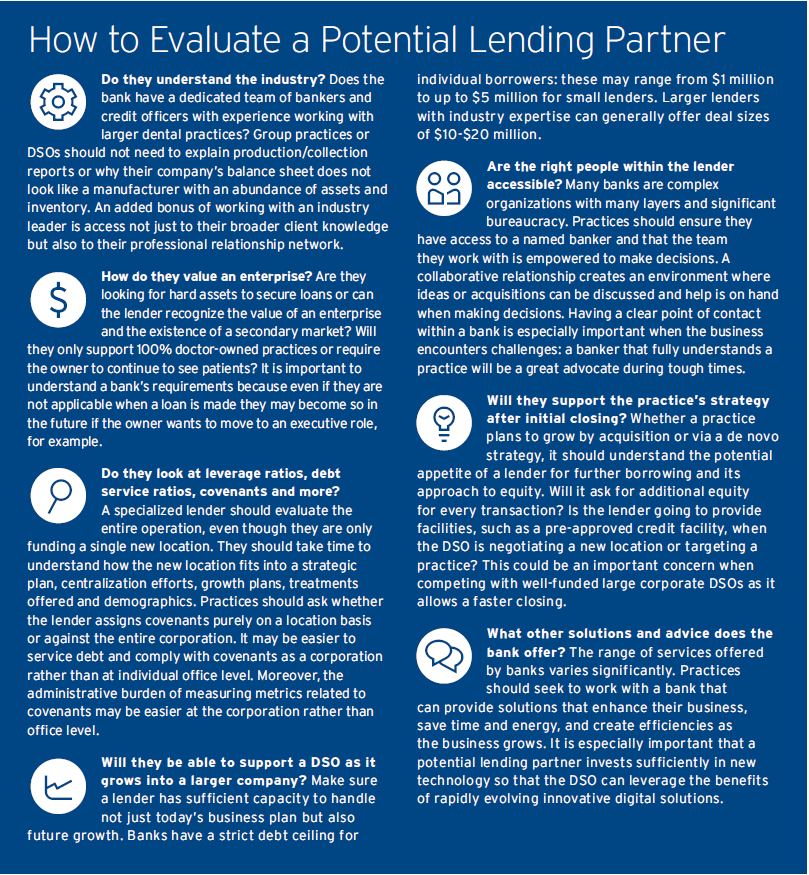

Choosing the Right Partner

The opportunities for group practice and DSOs are great.

The pace of financial innovation is accelerating as external business leaders and expertise enter the dental sector. This is freeing up dentists from management, HR, administration and re-imbursement tasks and allowing them to explore clinical breakthroughs and focus on their trade. As a result, outcomes are better for patients using these services.

However, the challenges for the middle market or emerging groups or DSOs are tangible, especially in accessing affordable and reasonably structured capital. Advice and support is needed if a DSO is to achieve its growth objectives in a financially prudent and secure way. Consequently, choosing the right financing partner is critical.

A lender must have highly specialized bankers if it is to successfully evaluate and support DSOs and group practices. These specialists must be able to understand risk and potential mitigants while having a view into the entire operation – they cannot focus on a single transaction. Middle market group practices and emerging DSOs seeking finance and support must evaluate lending partners carefully (see callout box) and prioritize those with proven thought leadership credentials. They need to work with bankers that engage with CEOs, CFOs and owners of DSOs and have the expertise and experience to be part of a DSO’s strategic planning process.

About the author: Gareth Petsch is the National Director for the Healthcare Practice Finance Division

of Citi Commercial Bank. His team of dedicated health care specialist bankers covers the US from New

York to California with a focus on group practice and DSO clients in the emerging/middle market segment.

Contact information: gareth.petsch@citi.com / 703.234.7315

Now, job seekers can post CVs and DSOs can fill

clinical and management jobs on JoinDSO:

If you found this article insightful or informative,

you’ll also enjoy GDN’s free monthly enewsletter: