Sponsored Content

Dentistry’s shift to a corporate model that’s more focused on efficiencies and margins is being driven by increased competition, elevated patient expectations, and outside investor interest. There are many ways in which DSOs and group practices finance their expansions, and choosing the right capital has become increasingly critical, writes Timothy Vandecar, Vice President for the Healthcare Specialty Finance Division at Citi Commercial Bank.

The ancient adage, “All roads lead to Rome,” rings true today with respect to the many avenues dental support organizations (DSOs) and group practices can take in financing their growth. However, not all paths chosen are likely to lead to the growth targets set by management, nor do all options fit the unique platform and plans of any one specific group practice or DSO. There are many nuanced drivers fueling the need for capital, but most can be aggregated into three primary drivers within the industry. These drivers are: capital expenditure (CAPEX) and platform development; mergers and acquisitions (M&A); and joint ventures and equity events.

Emerging and middle market group practices and DSOs are spending heavily on the CAPEX needed to support their platforms. These investments range from cutting edge clinical equipment and tools to IT and cloud-based software as a service (SaaS) that streamlines the patient-to-employee interface. Material investments are also being made for tenant improvements at acquired or de novo locations, as well as centralized space for the consolidation of non-clinical services. Investment in infrastructure, systems and platform development may continue as both emerging and middle market group practices and DSOs work to differentiate themselves via their unique platforms and value propositions.

The accelerating state of consolidation taking place within the dental industry is a factor driving the need for financing within the sector. Many smaller dental practices are being swept up by larger and increasingly sophisticated dental enterprises via acquisitions or mergers. The multiples of earnings before interest, taxes, depreciation and amortization (EBITDA) being paid by acquiring investors and these larger corporate dental operators can vary, but has increased in recent years for proven and established DSOs and group practices. The industry’s consolidation may well continue until what Harvard Business Review calls “Balance & Alliance” is achieved — that is, when the fragmented industry is fully consolidated with the top three market participants claiming 70% to 90% of market share, with established alliances to protect margins.1

The disruptive trends now taking place within the dental industry, which for more than a century had followed the same operating model, is spurring some clinicians to join forces through joint ventures. Many of these joint ventures (JVs) are being formed to create economic scale and protect the profitability of constituent smaller operators. Not all JVs, however, are created equal in the dental space: some are loose affiliations of practices; others are fully integrated platforms of many dental practices with partial to full centralization of non-clinical services. Many of these ventures require capital raises as part of an equity event which itself may create a new legal structure from which the joint owner clinicians can operate.

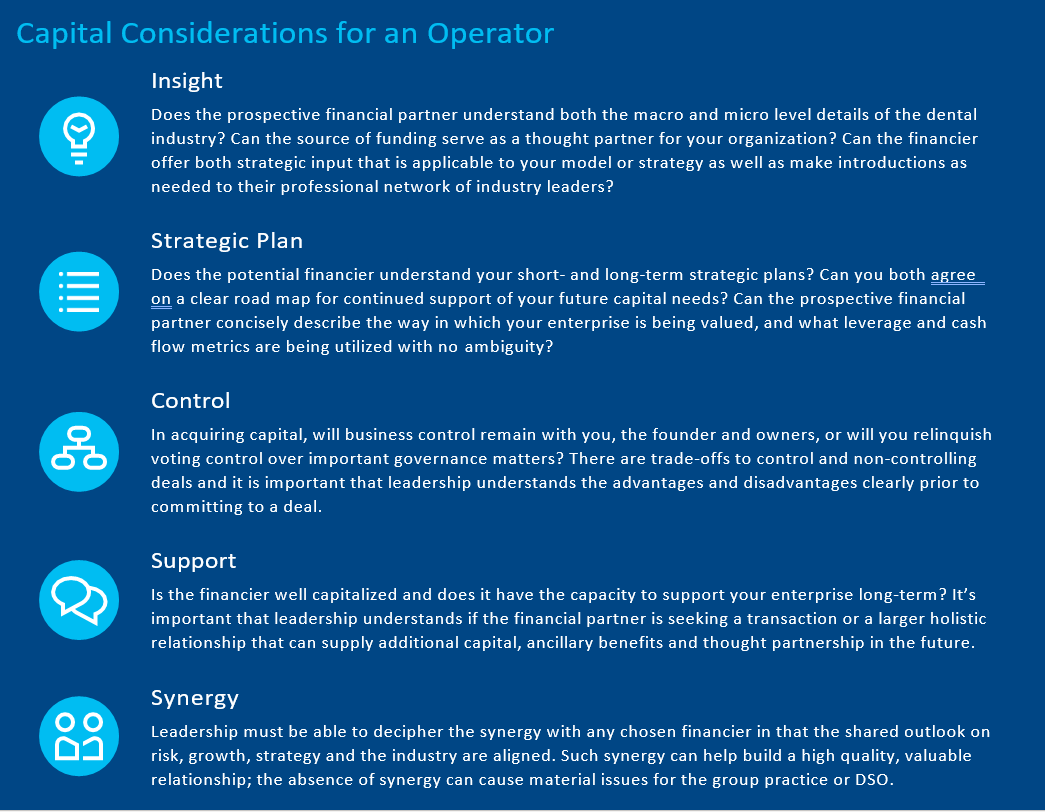

Types of Capital

Bootstrapping:

Bootstrapping, or pooling the personal funds of founders and owners in a DSO or group practice, can be a highly effective way to quickly supply needed cash when proving a concept or new platform, but it is not without its limitations and risk.

Many emerging group practices and DSOs lack the historic track record of an established corporate dental enterprise. This limitation can make it difficult to obtain traditional financing. By bootstrapping, an operator can focus on further developing a platform without the pressure of meeting outside investors’ performance benchmarks or a bank’s capital covenant requirements.

Bootstrapping can help an operator define its business strategy and vision without outside influences. Emerging dental enterprises that rely on bootstrapping, however, often have difficulty fully implementing segments of a platform due to cash constraints. Partial implementation of a platform’s various segments may help to obtain future outside capital investment interest.

Some of these partially implemented segments can include clinical and operational standards, a business development strategy, marketing, talent acquisition, HR, compliance, billing and financial reporting. Still, bootstrapping can put substantial personal financial pressure and risk on individual founders and owners and, furthermore, the cash they provide may not be sufficient to achieve the practice’s growth targets. Because of these pressures and risks, bootstrapping is generally not a long-term solution to scaling an enterprise.

The term bootstrapping can also be applied to operators that finance their expansion through excess operating cash flow. Such financing can have similar limitations to the use of personal funds in that the available excess cash flow may not be enough to successfully execute the growth strategy in a reasonable period of time. It’s for these reasons that operators may look to outside sources of financing to fund their expansion.

Equity Finance:

Equity finance has become increasingly common for scaled group practices and DSOs. The shift in mindset towards enterprise value and platform over the simple all-in-one solo dental office has launched the industry into unchartered territory that is equity finance, particularly private equity (PE).

Private equity has been attracted to the dental sector by its high margins, relatively unconsolidated practices, and the ability to streamline operations to create greater value. Owner clinicians often find themselves taking on private equity to access the capital they need to execute theirmnaggressive growth strategy and to gain operational expertise.

Accessing the cash needed to grow can be very attractive, but serious decisions need to be made by founders and owners before moving forward. First, not all PE firms are created equal with respect to industry experience and specialization. Owner clinicians should complete their due diligence on a prospective PE firm in order to make an informed decision on that firm’s capabilities. Second, different PE firms often have very different approaches to their roles: some may wish to take a back seat to the vision and plans set forth by the current leadership; others may prefer to take a direct hands- on approach; still others may require voting control of the enterprise. For these reasons, it is critically important that founders and owners understand the role a prospective PE partner would expect to play and then determine if the firm and its role are a good match.

In some cases, clinician owners will need to evaluate whether relinquishment of voting control to raise capital is consistent with their long-term vision and strategy for the enterprise.

Debt Finance:

Debt finance can be offered in many ways, from early forms that can equate to owner, family and friend financing, to more established financing from a commercial bank that specializes in the financing of DSOs and group practices.

The types of debt financing available to dental enterprises can vary by the enterprise’s development stage, profitability, structure and overall strategy. Bank financing can offer significant benefits to founders and owners who have their own long-term vision for the organization and who prefer not to relinquish equity control. Banks chosen to provide financing to emerging DSOs and group practices should specialize in the nuances of both the dental industry as a whole as well as the individual DSO or group practice to which it is providing capital. Founders and owners should be able to share their vision, strategy and target milestones with a prospective lender, and both should be able to come to an understanding of what the next 12, 24 and 36 months will look like with respect to CAPEX, M&A and de novo launches. Such bankers should also act as value-added thought partners to a group practice or DSO. This approach offers the benefit of professional industry insight as the DSO or group practice builds its strategic plans.

Bank financing, contrary to PE finance, requires no equity in exchange for needed capital and expertise. Beyond capital, a major differentiation of a DSO-specialized bank is in the suite of ancillary, but highly valuable, products and services that such a bank can offer, such as corporate credit cards for all levels of the enterprise, revenue cycle management products, such as lockbox for payer remittances and working lines of credit, depository accounts with earnings credit for liquidity and operational needs, and proprietary functions software such as patient payment portals that allow for ease of direct payment by patients to a DSO or group practice’s bank. A group practice or DSO needs to consider the covenant requirements a bank may require of the enterprise. The covenant requirements for capital should be prudent but allow the DSO or group practice enough flexibility to facilitate new targets, expansions and launches.

1 Graeme K. Deans, Fritz Kroeger, Stefan Zeisel, (2002, December) “The Consolidation Curve”

About the author: Timothy Vandecar is the Vice President for the Healthcare Specialty Finance Division of Citi Commercial Bank. His team of dedicated health care specialist bankers covers the US from New York to California with a focus on group practice and DSO clients in the emerging/middle market segment. Contact information: timothy.vandecar@citi.com / 858.260.0628

About the author: Timothy Vandecar is the Vice President for the Healthcare Specialty Finance Division of Citi Commercial Bank. His team of dedicated health care specialist bankers covers the US from New York to California with a focus on group practice and DSO clients in the emerging/middle market segment. Contact information: timothy.vandecar@citi.com / 858.260.0628

© 2019 Citigroup Inc. Citibank, N.A. Member FDIC. Equal credit opportunity lender. Citi, Citi and Arc Design and other marks used herein are service marks of Citigroup Inc. or its affiliates, used and registered throughout the world. 1792666 01/19

Looking for a Job? Looking to Fill a Job? JoinDSO.com can help: Subscribe for free to the most-read and respected

Subscribe for free to the most-read and respected

resource for DSO analysis, news & events: Read what our subscribers & advertisers think of us:

Read what our subscribers & advertisers think of us: